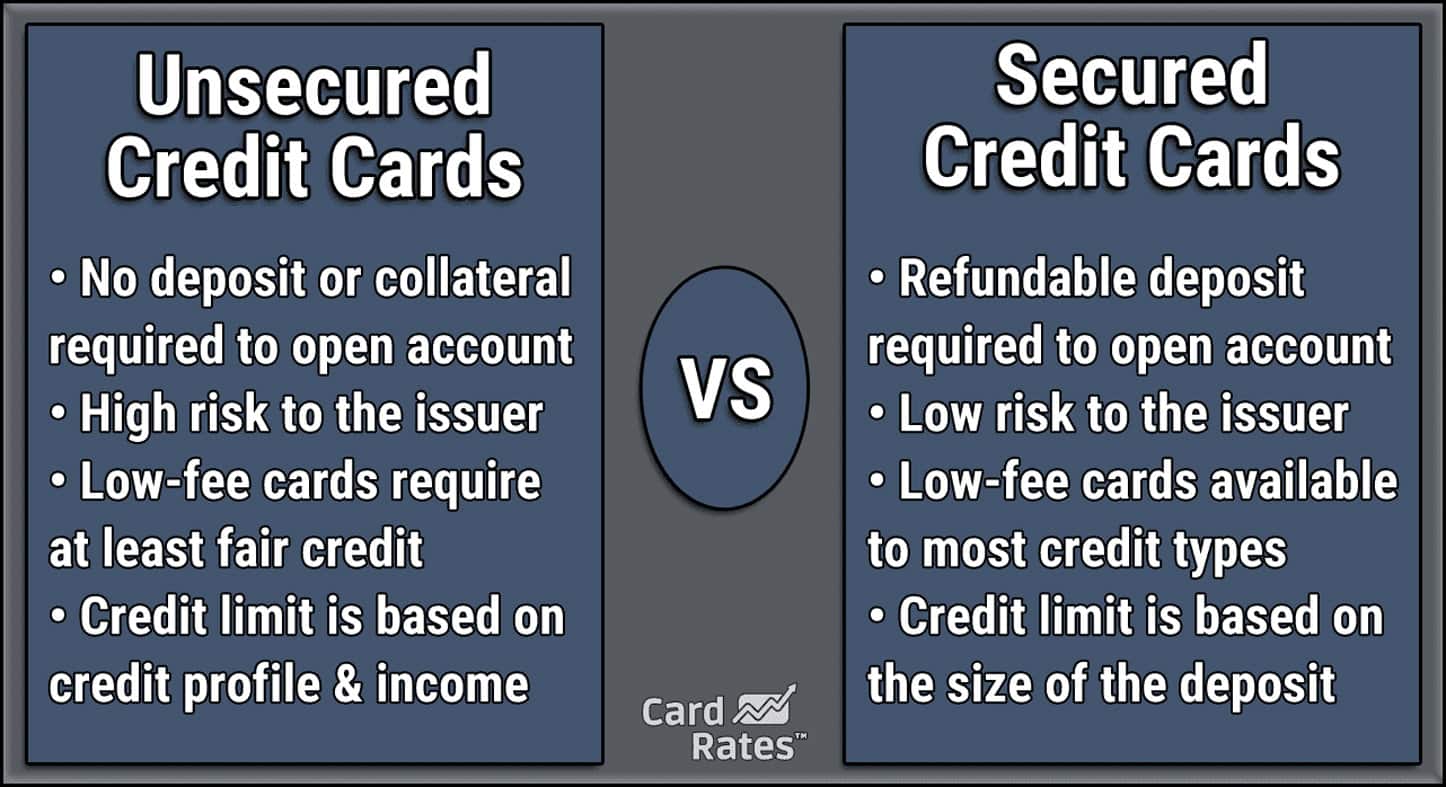

Advantages and you may Cons regarding a conventional Finance

If you’re given how exactly to finance your property get, the quantity of home loan models and you may financing alternatives makes your mind twist. It is tempting to direct straight to your loan alternative on the lower rates, but it’s really worth pausing to consider the choices in more detail, you start with a conventional loan.

Antique financing involve any type of home loan not supported by a good bodies service. They are made to be around for almost all homebuyers however, will often have more strict down-payment and you may borrowing from the bank standards than government-recognized financing. If you are in the market for a mortgage, antique fund are usually the first place to begin before you discuss other choices. Let us talk about the pros and you can downsides away from old-fashioned financing.

Much more Alternatives

Due to the fact antique finance are not supported by a national agencies, loan providers have significantly more liberty giving versatile selection with respect to mortgage rates, words and more. You should have way more versatility to determine if or not you desire fixed- otherwise changeable-price investment, and you will normally avoid the extra expense out-of home loan insurance rates for those who put down an enormous adequate amount (always 20%).

With a federal government-supported financing, mortgage insurance policy is have a tendency to incorporated, and you can speed and you will label alternatives can be even more restricted. Very bodies-backed fund additionally require the domestic you purchase towards the loan become your primary household. A normal mortgage enables you to avoid all these limits.

Higher Mortgage Restrictions

Having less regulators engagement entails you’ll be able to constantly manage to gain access to additional money which have a conventional mortgage. The newest restriction on an enthusiastic FHA loan, that’s one kind of regulators-recognized loan, already lies within $step 1,149,825 to possess highest-rates areas. To have a traditional loan, at the same time, you may even manage to use as much as $dos million in certain markets in case the credit score is high sufficient.

It is critical to remember that old-fashioned financing get into one or two classes: compliant and you may non-conforming. A compliant loan adheres to criteria, together with mortgage limitations, put from the businesses particularly Federal national mortgage association and you will Freddie Mac computer, and that purchase existing mortgages. The newest limitation to the an elementary compliant mortgage ranges off $766,550 to help you $step 1,149,825, based on in your geographical area. Certain areas ounts. If you prefer a larger compliant financing than what is offered in your area, you happen to be in a position to safer a non-compliant jumbo financing for as much as $2 billion, however, this could incorporate higher pricing plus difficult certificates.

If or not you choose a normal loan or not, considering your loan limit comes down to what you can afford. Check out our home value calculator to choose a good financing restriction for the disease.

Versatile Rates of interest

Antique loans could possibly offer alot more flexible rates, especially if you provides a robust credit rating. These types of funds and additionally carry less additional can cost you, including home loan insurance coverage or mortgage origination charges. Mainly because are less than with bodies-backed finance, your own full annual percentage rate (APR) – the fresh new yearly price of your loan, along with interest and you can fees just like the a portion of your own total financing amount – will usually become below which have a government-supported mortgage.

Down Financial Insurance Payments, otherwise Nothing at all

One of the biggest benefits associated with traditional loans is their liberty when it comes to individual home loan insurance (PMI). That is an extra fee you are able to pay on your monthly payment to help you offset the chance for your lender when you have less than simply 20% payday loan in Compo CT security of your property. Government-supported finance, which happen to be always good for homeowners that have a decreased down payment, generally speaking become mortgage insurance and will want it on complete life of the loan, even with you’ve built up more than 20% collateral.